This is an official version.

Copyright © 2010: Queen's Printer,

St. John's, Newfoundland and Labrador, Canada

Important Information

(Includes details about the availability of printed and electronic

versions of the Statutes.)

Newfoundland and Labrador

Regulation 2010

NEWFOUNDLAND

REGULATION 74/10

Cost

of Consumer Credit Disclosure Regulations

under the

Consumer Protection and Business

Practices Act

(O.C. 2010-232)

(Filed September 1, 2010)

Under the authority of section 83 of the Consumer Protection and Business Practices Act, the Lieutenant-Governor in Council makes the following regulations.

Dated at St. John's, August 30, 2010.

Gary Norris

Clerk of the Executive Council

REGULATIONS

Analysis

1. Short title

2. APR - fixed credit

3. APR - open credit

4. APR - no cost of borrowing

5. APR - leases

6. High ratio mortgage

7. Value given

8. Exemptions from the act

9. Initial disclosure statement for a mortgage

10. Calculation of prepayment refund or credit

11. Initial disclosure statement for fixed credit

12. Interest change disclosure

13. Mortgage renewal disclosure

14. Open credit disclosure

15. Lease disclosure

16. Lease maximum liability

17. Application for credit card

18. Commencement

Short title

1. These regulations may be cited as the Cost of Consumer Credit Disclosure Regulations.

2. (1) For the purpose of paragraph 45(1)(b) of the Act, the cost of borrowing for a loan under a credit agreement, that is a fixed credit, is to be expressed as an annual rate on the principal, as follows:

where

APR is the annual percentage rate cost of borrowing;

C is an amount that represents the total cost of credit;

P is the average principal outstanding over the term, being the sum of the principle outstanding during all calculation periods divided by the number of calculation periods in the term; and

T is the term of the loan in years.

(2) For the purpose of the

(a) the

(b) each instalment payment made on a loan shall be applied first to the accumulated cost of borrowing and then to the outstanding principal;

(c) a period of

(i) one month is 1/12 of a year,

(ii) one week is 1/52 of a year, and

(iii) one day is 1/365 of a year;

(d) if the annual interest rate underlying the calculation is variable over the period of the loan, it shall be set as the annual interest rate that applies on the day that the calculation is made;

(e) if there are no instalment payments under a

credit agreement, then the

(f) when a credit agreement is renewed, the outstanding balance immediately before renewal is regarded as an amount advanced to the borrower at the time of renewal, and advances and payments accounted for in that outstanding balance are otherwise disregarded.

3. (1) For the purpose of paragraph 45(1)(b) of the Act, the cost of borrowing for a loan obtained under a credit agreement, that is an open credit, is to be expressed as an annual rate, as follows:

(a) if the loan has a fixed annual interest rate, that annual interest rate; or

(b) if the loan has a variable interest rate, the annual interest rate that applies on the date of the disclosure.

(2) For the purpose of paragraph 45(1)(z) of the Act an index rate is a rate that is made public at least weekly in a publication that has general circulation in the province.

4. The

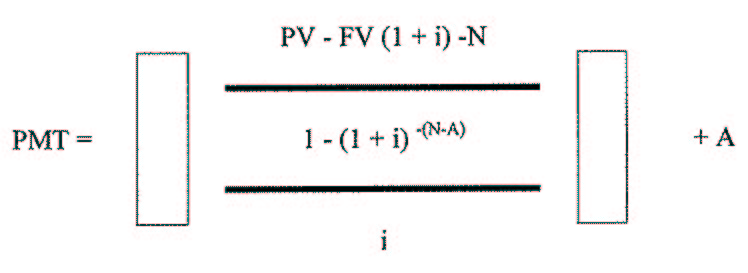

5. (1) For

the purpose of paragraph 45(1)(b) of the Act, the

where

M = the number of payment periods in a year;

i = the periodic interest rate such that

where

PMT = the amount of each periodic payment;

PV = the capitalized amount;

FV = the amount of the assumed residual payment;

i = the periodic interest rate;

N = the number of payment periods in the lease; and

A = the number of period lease payments that are paid at or before the beginning of the term.

(2) For the purpose of calculating the

(a) an amount payable by the lessee in respect of a tax may be treated as a payment only if an amount in respect of the tax was treated as an advance in calculating the capitalized amount; and

(b) a charge payable by a lessee may be treated as an advance only if an equivalent charge would be payable by a cash customer.

(3) Where the payments due under the lease vary in amount or are payable in relation to payment periods that vary in length, the equation referred to in subsection (1) shall be modified as necessary to calculate the value of "i" in accordance with actuarial principles.

(4) Where a lease is for an indefinite term or is

renewed automatically until one party takes steps to terminate it, the

(a) in the case of a lease that allows the lessee to automatically acquire title to the leased goods after a specified period of time, on the assumption that the term of the lease is that period of time; or

(b) in any case, on the assumption that the term of the lease is one year.

(5) For the purpose of the definition “capitalized amount” in paragraph 45(1)(h) of the Act, the amount of a payment made by the lessee at or before the beginning of the term does not include:

(a) a refundable security deposit; or

(b) a periodic payment.

High ratio mortgage

6. For the purpose of subparagraph 45(1)(s)(iii) of the Act, high ratio mortgage means a mortgage loan under which the amount advanced, together with the amount outstanding under another mortgage that ranks equally with or before the mortgage loan, exceeds 80% of the market value of the property.

Value given

7. For the purpose of paragraph 45(4)(c) of the Act, money transferred or to be transferred from the borrower to a person other than the credit grantor with respect to a charge for services that the credit grantor requires the borrower to obtain or pay for with respect to the credit agreement, unless the charge is for title insurance provided by an insurer chosen by the borrower, constitutes value given or to be given by a borrower with respect to a credit agreement..

Exemptions from the act

8. Part

(a) a sale of a service by a public utility as defined in the Public Utilities Act;

(b) a loan made by a life insurance company under a life insurance policy to the insured or his assignee solely on the security of the cash surrender value of the policy;

(c) a loan made under the Student Financial Assistance Act, the Canada Student Financial Assistance Act (

(d) the payment of taxes under the Municipalities Act, 1999; and

(e) overdraft protection on a deposit account.

Initial disclosure statement for a mortgage

9. (1) A credit grantor for a mortgage shall give an initial disclosure statement, in accordance with section 11, to each person entitled to disclosure, at least 2 business days before the earlier of the following:

(a) the day that the borrower first incurs an obligation to the credit grantor in relation to the mortgage; and

(b) the day that the borrower first makes a payment to the credit grantor in relation to the mortgage.

(2) Notwithstanding subsection (1), a person entitled to disclosure may waive the 2-day period and, in that case, the credit grantor shall give the initial disclosure statement to the person before the first occurrence of an event described in paragraph (1)(a) or (b).

(3) A waiver referred to in subsection (2) shall be in writing and signed by the borrower.

Calculation of prepayment refund or credit

10. The portion of each non-interest finance charge that shall be refunded or credited to the borrower under section 52(3) of the Act is determined by the equation:

C = U

x F

T

where

C = is the amount to be credited;

U = is the length of the unexpired portion of the term at the time of prepayment;

T = is the length of the period between the time the non-interest finance charge was imposed and the end of the term; and

F = is the amount of the non-interest finance charge.

Initial disclosure statement for fixed credit

11. (1) The initial disclosure statement for the purpose of subsection 47(2) and section 60 of the Act for a scheduled-payments credit agreement shall disclose the effective date of the statement and as much of the following information as applicable:

(a) for a credit sale, a description of the product;

(b) the outstanding balance as of the effective date of the disclosure statement, accounting for every payment made by the borrower on or before the effective date;

(c) the nature and amount of each advance, charge or payment accounted for in the outstanding balance disclosed under paragraph (b);

(d) the term;

(e) the amortization period, where it is longer than the term;

(f) the date on which interest begins to accrue and the particulars of a grace period;

(g) where the interest rate will not change during the term,

(i) the interest rate,

(ii) the circumstances under which unpaid interest will be added to principal, and

(iii) the application of payments as between interest and principal;

(h) where the interest rate may change during the term,

(i) the initial interest rate, the circumstances under which unpaid interest will be added to principal and the application of payments as between interest and principal,

(ii) the method of determining the interest rate throughout the term, and

(iii) unless the amount of scheduled payments is adjusted automatically to account for changes in the interest rate, the lowest annual interest rate, based on the initial outstanding balance, at which the payments would not cover the interest that would accrue between payments;

(i) the nature and amount of a charge, other than interest, that is not disclosed under paragraph (c) but that will be payable by the borrower in connection with the credit agreement;

(j) the amount and timing of an advance to be made after the effective date of the disclosure statement;

(k) the amount and timing of a payment to be made after the effective date of the disclosure statement;

(l) the total of all advances made or to be made in connection with the credit agreement;

(m) the total of all payments to be made in connection with the credit agreement;

(n) the total cost of credit;

(o) the

(p) the nature of a default charge provided for by the credit agreement;

(q) a description of the subject matter of a security interest;

(r) for a mortgage loan, a statement of the conditions under which the borrower may make prepayments, and a charge for prepayment;

(s) for a credit agreement other than a mortgage loan, a statement that the borrower is entitled to prepay the entire outstanding balance at any time without penalty and is entitled to make partial prepayments without penalty on a scheduled payment date;

(t) the nature of, and the amount and timing of payments for, an optional service purchased by the borrower for which a payment is to be made to or through the credit grantor; and

(u) the borrower's right to cancel an optional service of a continuing nature in accordance with section 51 of the Act.

(2) The initial disclosure statement for a credit agreement that is not a scheduled-payments credit agreement shall

(a) disclose as much of the information referred to in paragraphs (1)(a) to (c), (f) to (i) (1) and (o) to (u) as applicable; and

(b) either disclose the circumstances under which the outstanding balance, or a portion of it, shall be paid or refer to the provisions of the credit agreement that describe those circumstances.

Interest change disclosure

12. The information required to be disclosed for the purpose of subsection 61(1) of the Act is the following:

(a) the annual interest rate at the beginning and end of the period;

(b) the outstanding balance at the beginning and end of the period; and

(c) for a scheduled-payments credit agreement, the amount and timing of all remaining payments, based on the annual interest rate at the end of the period.

Mortgage renewal disclosure

13. (1) The information required to be disclosed for the purpose of subsection 64(2) of the Act is the following:

(a) the maturity date;

(b) the outstanding balance as of the maturity date, assuming that the borrower makes all the payments due between the date of the disclosure statement and the renewal date;

(c) the term of the renewed agreement;

(d) the amortization period from the renewed date;

(e) the relevant interest rate information referred to in paragraph 11(g) or (h);

(f) the nature and amount of a charge other than interest payable in connection with the renewed agreement;

(g) the amount and timing of all payments to be made in connection with the renewed agreement;

(h) the total of all payments to be made in connection with the renewed agreement;

(i) the total cost of credit for the renewed agreement;

(j) the

(k) a statement of the conditions under which the borrower may make prepayments, and a charge for prepayment.

(2) The disclosure statement may provide information regarding alternative renewal options offered to the borrower.

Open credit disclosure

14. (1) As much of the following information as applicable is required to be disclosed for the purpose of section 68 of the Act:

(a) the credit limit;

(b) the minimum periodic payment or the method of determining the minimum periodic payment;

(c) the initial annual interest rate and the compounding period;

(d) where the annual interest rate may change, the method of determining the annual interest rate at any time;

(e) when interest begins to accrue on advances or different types of advances, and the particulars of a grace period;

(f) the nature and amount, or the method of determining the amount, of a non-interest finance charge that may become payable under the agreement;

(g) an optional service purchased by the borrower for which a payment is to be made to or through the credit grantor, and the charges for the services;

(h) a description of the subject matter of a security interest;

(i) the nature of a default charge provided for by the agreement;

(j) how often the borrower will receive statements of account;

(k) where the borrower is required to pay the outstanding balance on each statement of account in full on receiving the statement:

(i) a statement to that effect,

(ii) the period within which the borrower shall pay the outstanding balance to avoid being in default, and

(iii) the annual interest rate that applies to an amount that is not paid when due; and

(l) a telephone number in accordance with subsection 69(3) of the Act.

(2) Notwithstanding subsection (1),

(a) the credit limit may be disclosed

(i) in the initial disclosure statement,

(ii) in the first statement of account, or

(iii) in a separate statement delivered to the borrower no later than when the borrower receives the first statement of account; and

(b) information

(i) about optional services and charges for those services, or

(ii) that relates to a specific transaction under the credit agreement

may be provided in the initial disclosure statement or in a separate statement delivered to the borrower before the services are provided or the transaction occurs.

Lease disclosure

15. (1) As much of the following information as applicable is required to be disclosed for the purpose of section 77 of the Act:

(a) that the transaction is a lease;

(b) a description of the leased goods;

(c) the term of the lease;

(d) the cash value of the leased goods;

(e) the nature and amount of other advances received or charges incurred by the lessee at or before the beginning of the term;

(f) the amount and purpose of each payment made by the lessee at or before the beginning of the term;

(g) the capitalized amount;

(h) the amount, timing and number of the periodic payments;

(i) the estimated residual value of the leased goods;

(j) for an option lease,

(i) how and when the option may be exercised,

(ii) the option price if the option is exercised at the end of the term, and

(iii) the method for determining the option price if the option is exercised before the end of the term;

(k) for a residual obligation lease,

(i) the estimated residual cash payment, and

(ii) a statement to the effect that the lessee's maximum liability at the end of the lease term is the sum of the estimated residual cash payment plus the difference between the estimated residual value and the realizable value of the leased goods;

(l) the circumstances under which the lessee or the lessor may terminate the lease before the end of the term and the amount, or the method of determining the amount, of a payment that that lessee will be required to make on early termination of the lease;

(m) where there are circumstances which the lessee will be required to make a payment that is not disclosed under paragraphs (a) to (l),

(i) the circumstances, and

(ii) the amount of the payment or the method of determining the amount;

(n) the implicit finance charge;

(o) the

(p) the total lease cost.

(2) The circumstances referred to in paragraph (l)(m) include unreasonable wear or excess use.

Lease maximum liability

16. (1) For the purpose of section 78 of the Act, the lessee's maximum liability at the end of the lease term is the sum of the estimated residual cash payment plus the difference between the estimated residual value and the realizable value of the leased goods.

(2) For the purpose of subsection (1), the realizable value of leased goods at the end of the lease term is the greater of

(a) the net proceeds for which the lessor disposes of the goods;

(b) 80% of the estimated residual value; and

(c) the estimated residual value minus 3 times the average monthly payment.

(3) Where the amount determined under paragraph (2)(a) is less than the greater of the amounts determined under paragraphs (2)(b) and (c), the realizable value is reduced according to the extend that the difference in the amounts is attributable to unreasonable wear or excess use, or to damage for which the lessee is responsible under the terms of the lease.

Application for credit card

17. The information required to be disclosed for the purpose of subsection 72(1) of the Act is the following:

(a) either

(i) the annual interest rate, if the interest rate is not a floating rate, or

(ii) the index and the relationship between the index and the annual rate, if the interest rate is a floating rate;

(b) the grace period, if there is one;

(c) the amount of a non-interest finance charge; and

(d) the date as of which the information referred to in paragraphs (a), (b) and (c) is current.

Commencement

18. These regulations come into force on March 3, 2011.

©Earl G. Tucker, Queen's Printer